Reading a title report isn't just about ticking a box. It's a methodical deep dive into the property's history, where you're looking for anything that could come back to haunt you. You’re essentially playing detective to verify true ownership, uncover financial claims like liens, and understand any restrictions that could limit what you can do with the property. This review is your safety net, ensuring the Dallas property you're about to buy is free from nasty surprises before you sign on the dotted line.

Why Your Dallas Title Report Is Non-Negotiable

Before we get into the weeds, let's be clear: this document is arguably the most critical part of your due diligence in real estate here in Dallas. Think of the title report as the property's complete biography—it lays out its legal history and current standing for all to see. It’s your best defense against inheriting someone else's problems, whether that’s a lingering debt, a surprise ownership dispute, or a hidden restriction that could derail your future plans.

In a fast-moving market like North Texas, being able to read and understand this report is a non-negotiable skill for any serious buyer or investor. It’s what stands between you and a potential financial or legal nightmare down the road.

To help you get oriented, here's a quick look at the main sections you'll encounter and what they mean for your Dallas property purchase.

Key Sections of a Dallas Title Report at a Glance

This table breaks down the essential parts of a title report. Think of it as your cheat sheet for understanding what each section is designed to do.

| Section Name | What It Tells You | Why It's Important in Dallas |

|---|---|---|

| Schedule A | The basic facts: who owns the property, the legal description, and the policy amount. | This is your reality check. It confirms you’re dealing with the actual owner and that the property you think you're buying is the one legally described. In sprawling areas like Dallas County, with its many subdivisions, getting the legal description right is absolutely critical to avoid boundary issues. |

| Schedule B-I | The requirements that must be met before the title company will issue your policy. | This is the title company’s "to-do" list. It often includes things like paying off the seller's mortgage, clearing existing liens, or getting certain documents signed. In Dallas, this might include verifying HOA dues are paid in full for neighborhoods like Lakewood or ensuring all property taxes owed to Dallas County are settled. |

| Schedule B-II | The exceptions—things your title insurance policy won't cover. | Pay close attention here. This section lists items that will remain on the title after you buy, such as utility easements, building restrictions, or mineral rights reservations. For Dallas buyers, this could reveal a pipeline easement that limits where you can build a pool or specific homeowner's association rules. |

| Plat Map | A visual map showing the property's boundaries, dimensions, and location. | This visual guide helps you understand the property's physical layout and its relationship to neighboring lots and public access points. It's especially useful for identifying easements or encroachments that might not be obvious from just walking the property line. |

Understanding these components is the first step toward a secure and confident real estate transaction. Each section provides a piece of the puzzle, and together they give you a complete picture of the property's legal health.

Protecting Your Investment

This report is your primary shield. The whole point is to identify and resolve any "clouds" on the title before you take ownership. These are the kinds of issues that can turn a great deal into a disaster:

- Unpaid Property Taxes: Any outstanding balances owed to Dallas County will become your problem.

- Mechanic's Liens: A claim filed by a contractor for unpaid work can stick to the property.

- HOA Liens: Unpaid dues or fines in communities like Preston Hollow or Turtle Creek can result in a lien.

- Ownership Disputes: Unresolved claims from previous owners, ex-spouses, or heirs can call your ownership into question.

A clean title report is the bedrock of a secure real estate purchase. It transforms a potential risk into a confident investment by confirming the seller has the undisputed right to transfer the property to you, free and clear of any surprise claims.

Ultimately, the title report provides the roadmap for the title company to issue a title insurance policy. If you want to dive deeper, you can learn more about what is title insurance in our detailed guide, which explains how this one-time purchase protects you from past events. Without a careful review of the report first, you're essentially buying blind.

Getting to Know Schedule A: The Property's ID Card

Once you get past the cover page, Schedule A is the first real meat of the title report. I always think of it as the property's official identification card. It lays out the most fundamental facts of the transaction, and getting these details right isn't just a formality—it's the bedrock of the entire deal.

Right at the top, you'll see the effective date. This is your snapshot in time. It tells you the exact moment the public records search concluded. Anything filed with Dallas County after this date and time, like a contractor filing a last-minute lien, won't show up.

The effective date is crucial because it sets the boundary for the title search. You'll want to make sure it’s recent. A stale date means you’re flying blind to potential issues that could have popped up since the search was done.

Is the Seller Who They Say They Are?

After checking the date, my eyes jump straight to the vested owner section. This is where you confirm who legally owns the property. The name listed here needs to perfectly match the seller's name on your purchase agreement. I can't stress this enough—there's no room for "close enough."

I once had a Dallas deal nearly fall apart over this. The contract listed the seller as "Johnathan Doe," but the title report showed the owner was "Johnathan Doe, as Trustee of the Doe Revocable Trust." It seems like a tiny detail, but legally, the trust owns the property, not Johnathan Doe the individual. We had to amend the contract and halt everything to verify the trust documents, causing a delay.

Always put Schedule A and your purchase contract side-by-side to compare the owner's name. A missing middle initial, a "Jr." that should be a "Sr.," or an LLC name instead of a personal one can bring the closing process to a screeching halt.

Pinpointing the Property with the Legal Description

Finally, you’ll find the legal description. This isn't the street address you use for pizza delivery. It's a much more formal, precise definition of the property's boundaries, and it will look something like this: "Lot 5, Block B, of the Highland Park Addition, an addition to the City of Dallas, Dallas County, Texas, according to the map or plat thereof…"

This dense language is what legally identifies the piece of land you're buying.

- Match it to the survey: Pull out your property survey and make sure the legal description on it is identical to what's on the title report.

- Look for typos: A single incorrect digit in a lot or block number could mean you're technically buying the lot next door. It happens!

- Trace the ownership history: Property can change hands in various ways, sometimes creating confusion on the title. To learn more about one common method of transfer, you can check out our guide on what is a quitclaim deed.

Giving Schedule A a thorough, detail-oriented review is your best first line of defense. It ensures the basic facts of your Dallas property purchase are locked in and correct from the get-go.

Navigating Schedule B: Uncovering The Red Flags

If Schedule A is the property's ID card, think of Schedule B as its detailed background check. This is where the real detective work begins. It lists all the "exceptions"—the specific things your title insurance policy will not cover once you own the property.

Frankly, skipping over this section is one of the biggest and most costly mistakes I see Dallas buyers make. Each item listed here is a potential restriction or encumbrance that could dictate how you use and enjoy your property down the road. Some are completely standard, but others can be serious red flags.

Standard Exceptions vs. Alarming Red Flags

Schedule B exceptions really fall into two buckets. First, you’ll see the standard, almost boilerplate items that show up on pretty much every title report in Dallas. These are generally low-risk.

Then you have the property-specific exceptions. These are tied directly to the history of the specific lot and building you’re buying. They can range from a minor note about a utility line to a deal-killing lien.

A clean title report is the bedrock of a secure transaction, and lenders in Dallas absolutely require it. In the competitive Dallas commercial real estate market, a solid title report is non-negotiable for vetting financial and legal risks before an acquisition.

My advice? Pay close attention to every single exception, even the ones that look standard. Never just assume an item is "normal" without understanding exactly how it impacts your specific Dallas property.

Common Schedule B Exceptions in Dallas and What They Mean

As you dig into Schedule B, you’ll come across a few common items again and again. It's crucial to understand what they are and, more importantly, what they mean for you as the new owner.

Let's break down some of the most frequent exceptions you'll find on Dallas-area title reports, their potential risks, and what you should do about them.

Common Schedule B Exceptions in Dallas and What They Mean

| Exception Type | Common Example in Dallas | Potential Risk | Recommended Action |

|---|---|---|---|

| Utility Easements | An easement granted to Oncor Electric Delivery to access power lines running along the back of a Lakewood property. | Low to Medium. Can restrict where you build a pool, fence, or addition. | Review the easement document to see its exact location and size. Ensure it doesn’t interfere with your future plans. |

| Deed Restrictions (CC&Rs) | HOA rules in a planned community like Viridian that dictate fence height, exterior paint colors, and satellite dish placement. | Medium. Violating these rules can lead to fines or forced compliance. | Request and thoroughly read the full CC&Rs document. Make sure you can live with the rules before closing. |

| Mineral Rights Reservations | A previous owner of a property in Frisco reserved the rights to any oil or gas found beneath the surface. | Low to High. In rare cases, this could grant a third party the right to conduct drilling operations on your land. | This is very common in Texas. Understand that you won't own the minerals. Ask the title company if there is any current production on or near the property. |

| Mechanic's Liens | A contractor files a lien on a Preston Hollow home after not being paid for a $50,000 kitchen remodel. | High. This lien must be paid. If it's not resolved by the seller, it could become your debt or cloud your title. | This is a deal-stopper. Insist the seller pay off the lien and provide proof of payment before you close. |

-

Utility Easements: This is probably the most common exception you’ll see. It simply gives utility companies the right to access a part of your property to maintain their equipment. It's usually no big deal, but a poorly placed easement could derail your plans for that dream pool.

-

Deed Restrictions and Covenants (CC&Rs): These are especially common in planned communities or historic districts like the M Streets. They're the rules of the neighborhood—governing everything from the color you can paint your front door to where you can park your RV.

-

Mineral Rights Reservations: Welcome to Texas! It’s incredibly common for a previous owner to have held onto the rights to any minerals under the land. This means someone else could potentially have the right to explore for oil or gas on your property.

-

Mechanic's Liens: This one is a major red flag. If a contractor did work on the property and never got paid, they can file a lien against it. That lien has to be settled before you can take clean ownership. To learn more about uncovering these kinds of historical claims, check out this guide on how to research property history.

Here’s the key takeaway: for every single document referenced in Schedule B, you need to request a copy from your title company. Reading the one-line summary isn't enough. You have to see the original documents to grasp the full picture and how each exception might affect your future.

Spotting Liens and Financial Claims

Once you've worked through the standard exceptions in Schedule B, it's time to zero in on what is arguably the most critical part of the report: financial claims. These are the liens and monetary burdens tied to the property, and if they aren't cleared before you close, they can quickly become your problem. This is where the real bombshells are often found.

Not all liens are the same, and it’s important to know what you’re looking at. They fall into a couple of main buckets, each with its own story and implications for the Dallas property you want to buy.

Voluntary vs. Involuntary Liens

The most common lien you’ll see is a mortgage or a Deed of Trust. This is a voluntary lien—the current owner willingly used the property as collateral for a loan. Seeing this is completely normal. The seller's loan will be paid off at closing from the sale proceeds.

Involuntary liens, on the other hand, are a different beast entirely. These are slapped on the property without the owner's consent, and they scream "red flag." They point to unresolved debts or legal fights that need to be sorted out immediately.

Any involuntary lien is a potential deal-killer. These must be paid in full and legally released by the seller before you get to the closing table. Never just assume the seller has a plan to handle it—demand proof that it's been resolved.

Here in Dallas, these liens typically pop up from a few common sources:

- Tax Liens: The IRS or Dallas County can file these for unpaid property or income taxes.

- Mechanic’s Liens: This is a claim made by a contractor who did work on the property but never got paid.

- Judgment Liens: These come from a lawsuit. If the owner lost a court case and owes money, the court can place a lien on their property. You'll find these filed at the Dallas County courthouse.

- HOA Liens: A homeowners' association can levy a lien for unpaid dues, fines, or fees.

A Real-World North Dallas Example

Let's say you're buying a property in a planned community in North Dallas. Your title report comes back and, buried in Schedule B, you see a $5,000 lien from the local HOA. It turns out the seller got into a dispute over landscaping rules and just decided to stop paying their dues.

If this isn't taken care of, that lien doesn't just vanish when the property sells. It stays with the house.

After you close, the HOA could come knocking on your door demanding that $5,000. In a worst-case scenario, they could even start foreclosure proceedings against you. This is exactly why you must object in writing, demand the seller pay the lien in full, and insist that the HOA provides a formal, recordable release to the title company before you sign a single document.

This process of uncovering financial traps is a core reason why you need to know how to read a title report. But spotting the problems is only half the battle. As a Dallas buyer, you also need to protect your investment from any title issues—both the ones you find and the ones that might still be hidden. This is where understanding the importance of title insurance comes in; it's the safety net that shields you from these exact kinds of financial headaches.

Creating Your Post-Review Action Plan

Finding a red flag on a title report isn't the end of the road. Think of it as a fork in the road—it’s time to take action. Reading the report is just the first half of the equation; how you respond to what you find is what protects your investment in Dallas.

Discovering a lien or a murky easement isn't enough. You have to move quickly and strategically within the timeframes laid out in your Texas real estate contract. This is where you turn what you've learned into real leverage for a smooth, secure closing.

Formulate Your Questions and Objections

Your first move should be to draft a clear, specific list of questions for your escrow officer. Vague inquiries will only get you vague answers.

Instead of asking, "What's this easement about?" try this: "Could you please pull the recorded document for the utility easement listed as Exception #5 on Schedule B? I need to understand its exact location and any restrictions on use."

That kind of precision is what gets you results. Your aim is to get your hands on the source documents for every single exception that gives you pause. From there, you'll work with your real estate agent to formally submit any objections to the seller in writing. This is a crucial step tied directly to your contractual timeline.

In Texas, if you miss your deadline to object to title issues, you’ve essentially accepted the title "as-is"—flaws and all. Don't let the clock run out on this. Treat it with the urgency it demands.

When to Bring in a Dallas Real Estate Attorney

Your agent and escrow officer are fantastic resources for most common title snags. But some problems are just too complex for them to handle alone. If your report reveals a break in the chain of title, a major boundary dispute, or an unreleased lien from a company that no longer exists, it's time to call a Dallas real estate attorney.

An attorney can dissect complicated legal jargon, gauge the actual risk involved, and map out your best course of action. That might mean negotiating a solution or, in some cases, walking away from the deal. This is particularly important for anything involving unresolved legal judgments filed at the Dallas County courthouse.

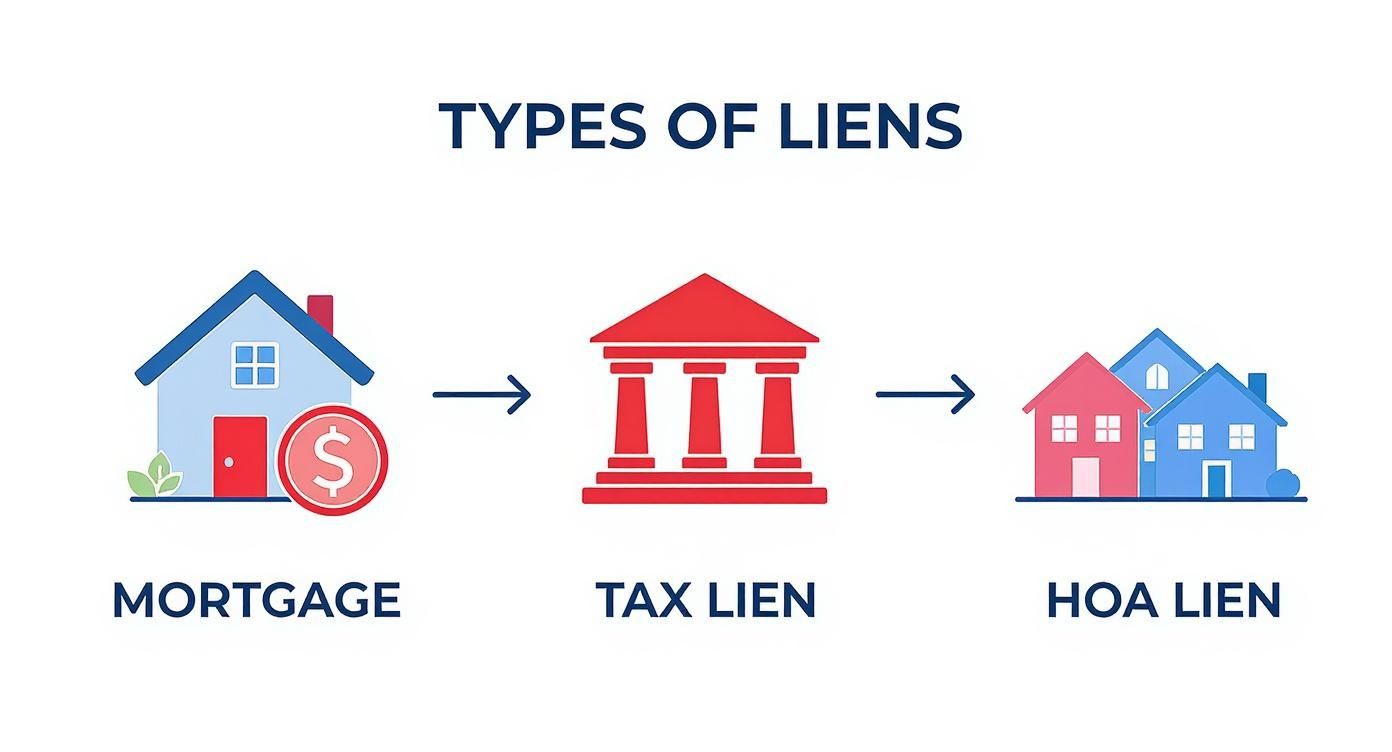

This infographic gives a great overview of the common liens you might run into.

As you can see, liens can be voluntary (like a mortgage) or involuntary (like unpaid taxes or HOA dues). Those involuntary ones are the ones that usually require immediate attention.

Negotiating a Clear Path to Closing

Once your objections are officially on the table, the real negotiations begin. The seller is generally on the hook to deliver a clean title, and you have every right to demand they do what it takes to make that happen.

Your action plan might look something like this:

- For Monetary Liens: Insist that the seller must pay off all tax liens, mechanic's liens, or judgment liens using their proceeds from the sale. The title company will need an official, recordable release for every single lien that gets paid off.

- For Easements or Restrictions: If the seller claims an easement is no longer valid, demand they provide proof that it has been legally terminated or resolved.

- For HOA Issues: Require a formal statement from the HOA confirming the seller’s account is paid in full and there are no outstanding violations tied to the property.

Building your post-review plan is all about proactive problem-solving. By asking the right questions, calling in legal help when you need it, and negotiating with confidence, you put yourself in the best position to arrive at the closing table in Dallas, ready to take ownership with a clean, unencumbered title.

Got Questions About Your Dallas Title Report? We've Got Answers.

When you're diving into a real estate deal in a market as hot as Dallas, the title report can feel a little overwhelming. Let's break down some of the most common questions that pop up during this crucial due diligence phase.

What's the Real Difference Between a Title Report and a Title Commitment?

You’ll hear these terms thrown around a lot, sometimes even used for each other, but there's a key distinction. Think of the title report (often called a preliminary report or "prelim") as the first look. It’s a snapshot of what the public records say about the property’s title right now. It's the fact-finding mission.

The title commitment, on the other hand, is the main event. This is the title company’s formal offer to issue a title insurance policy for your new property, but—and this is a big but—it’s based on you accepting the specific conditions and exceptions they list. In reality, the commitment is the document you and your agent will be working with to make sure any title issues are cleared up before you sign on the dotted line.

How Long Do I Have to Flag Any Title Problems?

Your window to object to any issues you find is spelled out in your real estate purchase contract. Here in Texas, the standard contract from the Texas Real Estate Commission (TREC) gives you a specific number of days for this review period.

The clock starts ticking the moment you receive the title commitment. It's on you to get any objections over to the seller in writing before that deadline hits.

Pro Tip: Don't let this deadline sneak up on you. Missing it is one of the biggest mistakes a buyer can make. If you let the objection period lapse, you’ve essentially agreed to take the property's title as-is, warts and all. Circle this date on your calendar immediately.

Can I Actually See the Documents Behind the "Exceptions"?

Yes, and you absolutely should. You have every right to see the full text of any recorded document that affects the property you're about to buy. It's not just a good idea; it's standard practice to request copies of every single underlying document listed as an exception in Schedule B.

What kind of documents are we talking about?

- The official plat maps for that new subdivision out in Frisco.

- The HOA Covenants, Conditions, and Restrictions (CC&Rs) for a property in a North Dallas planned community.

- The nitty-gritty details of a utility easement filed with Dallas County.

That one-line summary in the report won't tell you the whole story. Reading the source documents is the only way to truly understand how they could affect what you can (and can't) do with your property.

What if We Find a Major Problem That Can't Be Fixed?

This is exactly why you do this homework. If a serious title defect comes to light—say, a forged deed somewhere in the chain of title or a nasty boundary dispute with a neighbor—and the seller can't or won't fix it, your purchase contract is your escape hatch.

The contract will outline your options, but typically, this gives you the right to terminate the agreement. This is your protection, allowing you to walk away from a deal with a clouded title and, most importantly, get your earnest money back. It stops you from making a very risky investment.

Navigating the complexities of Dallas real estate requires a partner with deep local knowledge and a commitment to protecting your interests. At Dustin Pitts REALTOR Dallas Real Estate Agent, we guide clients through every detail of the transaction, ensuring a secure and successful purchase. Start your property search at https://dustinpitts.com.